EDGE #4 - The "Palantarization" of obsession with Arny Trezzi

In today's conversation I chat with Arnaldo (Arny) Trezzi on his investment and life philosophy, and how you can apply it to your professional ventures.

Big podcasts and large publications chase Bezos-level names who talk about strategy from 30,000 feet: it’s inspiring, yes, but useless if tomorrow you are walking into a meeting with your client and a deck to defend…

EDGE, a format by Consulting Intel, is where I sit down with world-class operators, consultants, and investors working between business, tech, and AI… and where I distill what I learn in something you can read in ~7 minutes.

LFG! 🔥

Imagine betting over 50% of your personal portfolio on a single, highly-controversial stock, only to see it crater… and then double down.

That is the philosophy of Arnaldo (Arny) Trezzi, a contrarian investor (and a fellow Italian) who sees market panic as his primary hunting ground.

Arny’s entire investment framework is built on a single, surprising claim: The obsession you develop for a company is your single greatest competitive advantage.

He believes traditional financial analysts are often “fools” for relying solely on quantitative models, missing the fundamental edge that comes from understanding a business’s culture, leadership, and underlying narrative better than 99% of the market.

By the way, using NotebookLM I have created a 4-minute video that visually explains the key concepts of my conversation with Arny: have a look!

Arny Trezzi is an independent investor and the founder of popular newsletters Palantir Bullets (focused exclusively on Palantir) and Arny Trezzi (more recent, covering other high-conviction theses). With a background in Investment Banking and as a generalist equity analyst at the start of his career, he is an admitted obsessive-compulsive who operates outside the traditional fund structure, focusing on a few companies he knows so well he can preemptively debunk every bear case.

Let’s jump into the conversation!

Origin Story

Arny began his academic journey in Italy studying Economics and Commerce, later switching to Banking and Finance, driven by a fascination with the psychological component of the stock market: the panic, the emotion, and the opportunities that arise when others are losing their calm.

The major turning point came after his undergraduate degree when he read The Intelligent Investor. The book shifted his focus away from portfolio management and quantitative risk models toward an entrepreneurial approach to investing, rooted in deep business analysis - a skill he realized he sorely lacked despite graduating with honors.

A key failure that cemented his conviction was his attempt to open an investment holding company with a partner, which failed due to “personal incompatibilities.” This left him unemployed with a resume that traditional financial institutions viewed as too rebellious.

When COVID hit, freezing hiring, he faced a fork in the road.

Instead of despairing, he chose to reorient himself during the market crash, seeing the widespread fear as an opportunity to test his newfound conviction by aggressively buying into companies like Amadeus and Apple, whose stocks were hit by short term narratives.

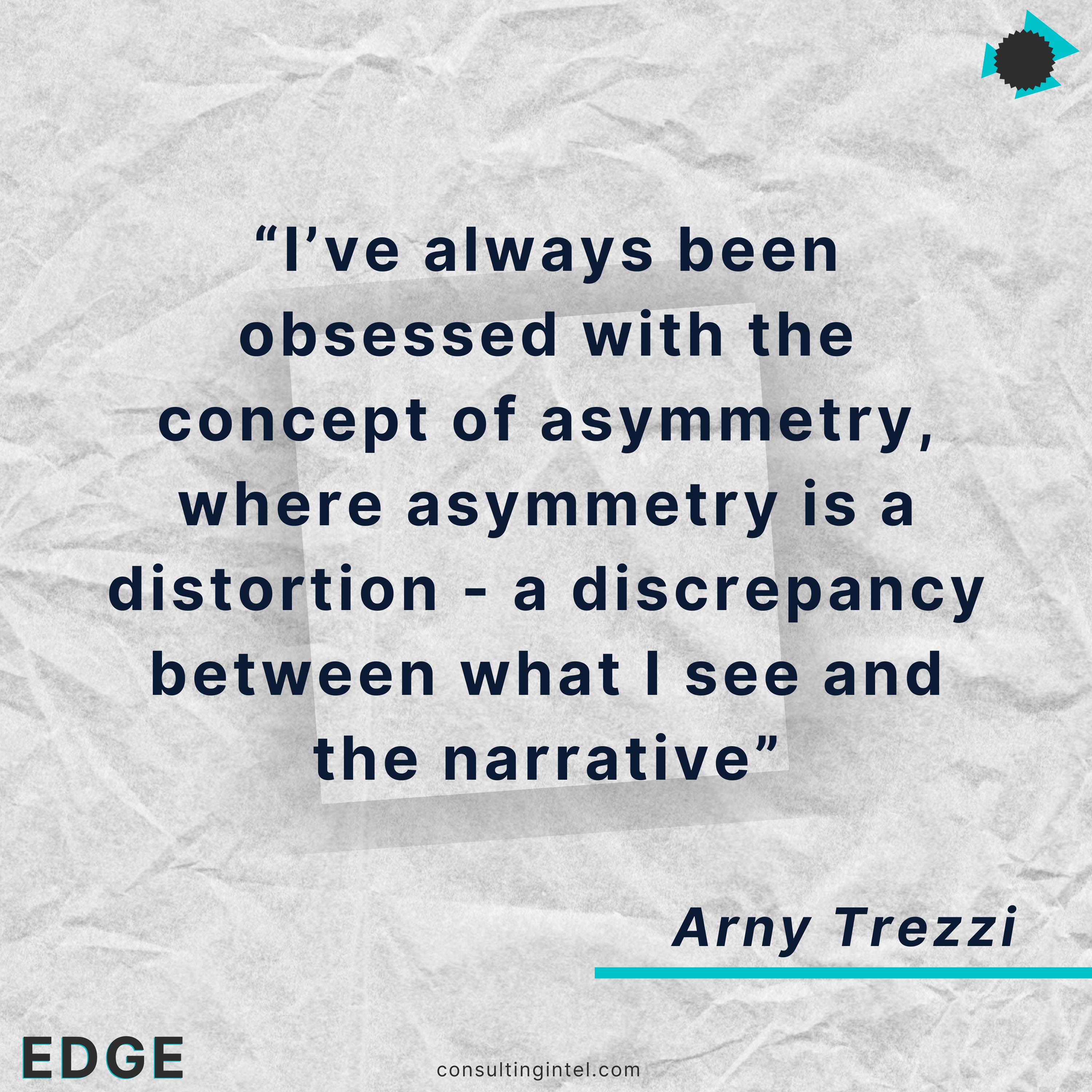

The belief that emerged from these experiences is that true Margin of Safety is not just a mathematical concept but an informational asymmetry you create. He focuses maniacally on “capturing the asymmetry” between the depressed or misunderstood market narrative and the positive reality of the underlying business.

Edge

Arny’s investment style is defined by an obsession with depth over breadth.

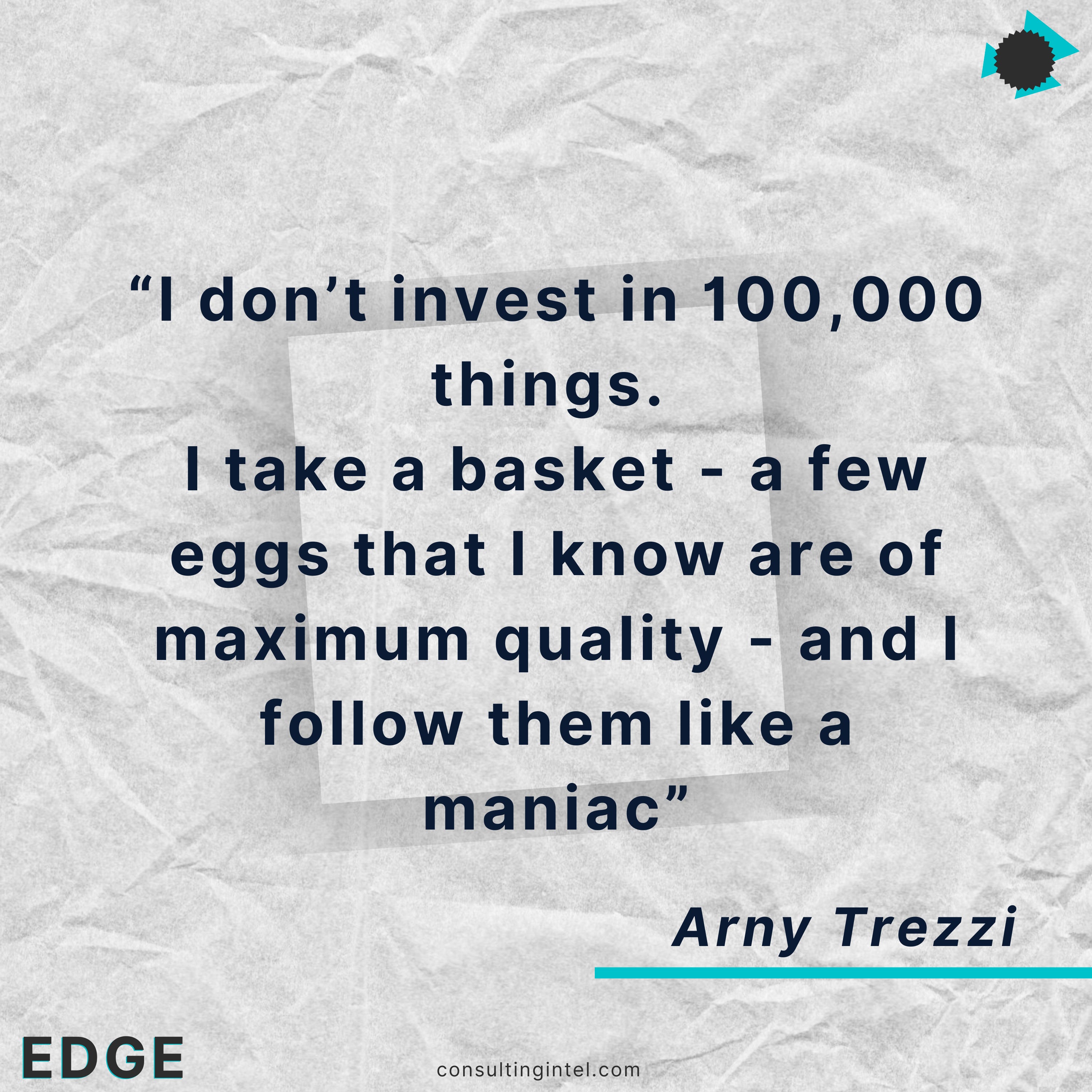

He fundamentally rejects the structured process of a traditional fund manager, which aims to find a good idea. Instead, he starts with a few select companies he is passionate about and wants to study - his “basket of high-quality eggs.” His goal is to deepen his “circle of competence” to the point where he can confidently say he is in the “top 1 percentile of business understanding” for those companies.

His philosophy was forged in his investment in Palantir, an obsession that still constitutes over 50% of his portfolio and generated him over 20x return in three years. He initially heard of Palantir when it was private but went “all in” when the stock dropped below $10 amidst peak pessimism. He shared his research online, receiving torrents of criticism, which he used as fuel.

“You’ve truly understood a company when you are able to take every possible criticism and, rationally and calmly, demonstrate how that criticism is actually a non-existent point.”

For Arny, this was a moment of “unhuman asymmetry.”

He had accumulated so many hours of study that he saw the positive, accelerating developments in the business that the market narrative was completely missing. He wasn’t looking for a quick flip: he was accumulating conviction to hold through volatility.

His approach has succeeded in finding value in both Palantir PLTR 0.00%↑ and Robinhood HOOD 0.00%↑, companies where the stock was depressed despite strong underlying business developments and culture.

Robinhood, Arny’s second biggest position after a 10x return, followed a similar initial recipe: loved by customers, hated by Wall Street. Arny believes his concentrated approach could be expanded to private markets, where he invested as an angel investor in Pillar, vertical SaaS for Real Estate, and participated in the latest round of Bending Spoons, the Italian first decacorn.

However, he emphasizes the limit of quantitative models: while the DCF model is useful for “testing your awareness,” it must never be mistaken for reality (citing his early mistake with Tesla TSLA 0.00%↑, which he recognized as a powerful business but felt was “unbuyable” based on his rigid model).

He must also always be aware of the Bear Case, but only invests when he is certain the risks are already incorporated into the price.

“I don’t invest in 100,000 things. I take a basket, a few eggs that I know are of maximum quality, and I follow them like a maniac.”

Future

Arny views the explosion of AI and Large Language Models (LLMs) as a major filter for the investment world. He believes LLMs are just a tool that can facilitate counter-thesis research, but they don’t change his structural approach.

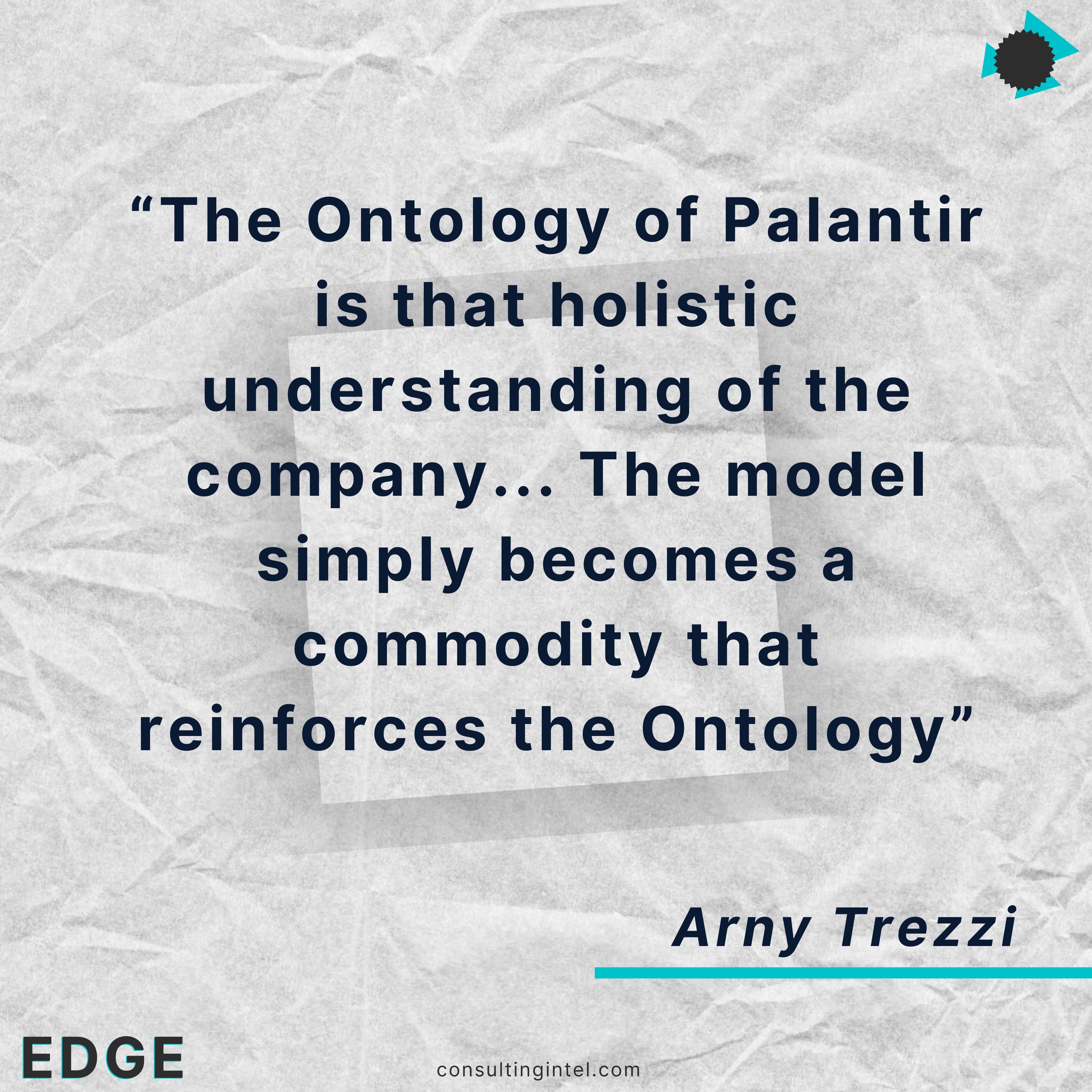

Arny’s investment thesis on Palantir is centered on the concept of Ontology. He sees Palantir not as a services company, but as a product company that used 20 years of services experience to build the world’s most powerful software platform.

His key prediction is: Palantir is the “operating system for using AI” in the enterprise, and the LLMs themselves are a commodity (the fuel). The real value is Palantir’s Ontology, which provides a holistic, digital twin understanding of the entire company, turning all the outputs of the LLMs into actionable knowledge that compounds within the firm.

He is concerned that LLMs will create a “false sense of confidence,” allowing people to generate investment theses in three hours instead of two weeks.

This shortcut is dangerous because, in his view, it takes a month to truly start understanding a company, and months more for those ideas to “ferment” and overcome confirmation bias.

Grounding and Legacy

Arny’s primary practice for mental clarity is intense physical exercise - specifically, calisthenics 2-3 times a week, and most crucially, “pushing himself to the limit in the mountains” (he is based near the Italian city of Lecco). He finds that this intense physical necessity forces his mind out of negative thought loops and restores the mental lucidity he needs as an investor.

Asked what project he would launch with unlimited time and resources, Arny admits he is currently in a position where the financial urgency is gone.

His priority has shifted to the personal realm: figuring out how to structure his life and compound value outside of just the financial channel.

This answer reflects his philosophy that once a certain financial threshold is crossed, the true value moves to time and experiences.

He notes the importance of “compounding in real life” and ensuring a stable personal foundation before tackling large entrepreneurial endeavors, citing the need to have a “fixed life” to be able to fully engage in an entrepreneurial “new leg.”

🔹 What you can steal

Arnaldo Trezzi’s philosophy offers powerful, actionable lessons for investors and business people alike. Let me summarize my key take-aways:

Inverse Your Research Framework: Stop trying to find the best idea by following a structured process. Instead, choose the two or three companies you are genuinely passionate about and whose developments you are excited to follow. Let your passion dictate your focus; the competence will follow.

Analyze the CEO and Culture Before the Numbers: Do not lead with the spreadsheet. Focus on understanding the CEO and the company culture first: Arny has met Palantir employees who accepted substantial pay cuts to work there (he also bumped into Alex Karp a couple of times in some Palantir events in the USA). Culture determines success, business translates culture into numbers, and numbers are the last piece of the puzzle .

Become Your Own Bear Case: Use criticism not as an attack, but as a roadmap. Actively seek out the strongest counter-arguments against your thesis. You must be able to rationally and calmly dismantle every single one to achieve true conviction and be confident that the risks are already incorporated into the stock price.

🔹 Maurizio’s Take

Arny is not a value investor in the traditional sense. He is an Information Arbitrageur.

In my view, his “obsession” is simply the modern-day moat for a solo investor. In a world saturated with financial data and models, the only way to gain a true informational edge is through sheer, cumulative time spent on a single target. He has successfully taken the consultant’s lens - prioritizing leadership, culture, and holistic business process (the Ontology) - and applied it to generate alpha where quantitative analysts, who are paid to look backward, fail.

The deepest takeaway is that your investment conviction is only as strong as the work you put in to defeat the bear case. If you let an LLM write your thesis in three hours, your conviction will evaporate in three minutes when the market panics.

This is true in investing, but I will leave it as an exercise for the reader to come up with an equivalent analogy in your professional field of play: it won’t take long.

The greatest risk in the age of AI isn’t not using the new tools, but using them to substitute the important, time-intensive process of truly digesting a company.

👀 Where to find more about Arny

If you enjoyed today’s conversation and read Consulting Intel, please do me a favor: share this post, spread the edge.

👋

Disclaimer: The views and opinions expressed above are current as of the date of this document and are subject to change without notice. Materials referenced above will be provided for educational purposes only. None of the above will include investment advice, a recommendation or an offer to sell, or a solicitation of an offer to buy, any securities or investment products.

⚠ Check these links out

My first book Beyond Slides became a #1 Amazon Best Seller in the USA, UK, Australia and Italy;

The Leaders Toolkit is a deck of 52 tools, frameworks and mental models to make you a better leader (use code CONSULTANT10 for 10% off);

The Consulting Intel private Discord group with 250+ global members is where consultants meet to discuss and support each other (it’s free).

« If you let an LLM write your thesis in three hours, your conviction will evaporate in three minutes when the market panics. » Bravo Maestro

Great write up! Thanks